Summary

From April 2025 to April 2026, China's yellow phosphorus prices experienced volatile upward movement before peaking and retreating in April 2026. During the spring farming supply guarantee period, phosphate fertilizer exports were fully suspended, combined with resumption of production in major producing areas leading to increased supply, putting downward pressure on yellow phosphorus prices from their highs. Based on data from the General Administration of Customs, industry associations, and market institutions, this article systematically analyzes phosphate fertilizer export data, yellow phosphorus price trends, corporate operating rates and inventory changes, and provides an outlook for the future.

I. Spring Farming Supply Guarantee Concludes: Adequate Phosphate Fertilizer Supply, Export Window Closed

The spring farming fertilizer supply guarantee for 2026 has largely concluded. According to statistics from the China Phosphate Fertilizer Industry Association, during the spring farming period from October 2025 to April 2026, phosphate fertilizer supply (in terms of P₂O₅) exceeded 8.5 million tons, far exceeding actual demand and fully meeting spring farming needs. From January to February 2026, cumulative production of diammonium phosphate (DAP) reached 2.57 million tons, up 1.6% year-on-year; cumulative production of monoammonium phosphate (MAP) reached 2.858 million tons, up 0.9% year-on-year, indicating steady production growth.

From a supply-demand balance perspective, overall fertilizer supply during spring farming was guaranteed, but phosphate and potash fertilizer supplies were slightly tight. A report in Farmers' Daily noted that major domestic phosphate fertilizer producers generally maintained sulfur inventories equivalent to 1.5–2.5 months of consumption, basically meeting production needs during spring farming. Wang Ying, Deputy Secretary-General of the China Phosphate Fertilizer Industry Association, stated that the phosphate fertilizer industry operated steadily in 2025, with output growing 4.9% year-on-year and product structure continuing to optimize. Notably, the rapid development of the new energy sector has injected new momentum into the phosphate fertilizer industry —in 2025, the capacity of industrial-grade monoammonium phosphate reached 5.5 million tons, of which 50% of consumption flowed to the new energy sector.

On the export policy front, to prioritize domestic fertilizer demand, phosphate fertilizer exports were fully suspended during spring farming. In March 2026, the General Administration of Customs urgently enforced a full suspension of phosphate fertilizer and phosphorus-containing fertilizer exports. After March 14, no new export inspection applications were accepted, and goods already declared but not yet released were denied clearance. The ban remains in effect until August 31.

II. Export Data: Sharp Drop in Phosphate Fertilizer Exports, Stable Yellow Phosphorus Exports

Phosphate fertilizer exports: Significant contraction under the ban.

According to China Customs statistics, from January to March 2026, China exported a total of 8.162 million tons of various fertilizers, up 14.1% year-on-year, with export value reaching USD1.76 billion, up 22.6% year-on-year. However, under strong policy control for supply assurance, phosphate fertilizer export volumes fell sharply.

For diammonium phosphate (DAP), cumulative exports from January to March 2026 were only 19,000 tons, a decrease of 59,000 tons compared to the same period last year, a drop of 75.6%. The average export price was USD733.8/ton, up USD116.4/ton or 18.9% year-on-year. March exports were zero, with only small amounts exported in January and February. For monoammonium phosphate (MAP), cumulative exports reached 111,000 tons, an increase of 78,000 tons or 231.7% year-on-year. The average export price was USD610.5/ton, down USD91.7/ton year-on-year. In March, MAP exports were 24,000 tons, down 61.3% month-on-month.

Yellow phosphorus exports: Limited in scale, generally stable.

Looking at export destinations, in the first quarter of 2026, DAP was mainly exported to Vietnam, Pakistan, and Bangladesh; MAP was mainly exported to Brazil (82,000 tons), Taiwan (China), Australia, and Indonesia, with these four destinations accounting for 89.5% of total MAP exports.

Reviewing full-year 2025 data, cumulative DAP exports reached 3.48 million tons, down 23.8% year-on-year; cumulative MAP exports reached 1.88 million tons, down 6.3% year-on-year. The average export price of MAP was USD660.6/ton, up USD127.0/ton or 23.8% year-on-year; the average export price of DAP was USD703.3/ton, up USD169.0/ton or 31.6% year-on-year. The upward trend in export prices reflects a tight global supply of phosphorus resources.

| Product | 2025 Q1 ('10,000 tons) | 2026 Q1 ('10,000 tons) | YoY Change |

| DAP (Diammonium Phosphate) | 7.8 | 1.9 | -75.60% |

| MAP (Monoammonium Phosphate) | 3.3 | 11.1 | 236% |

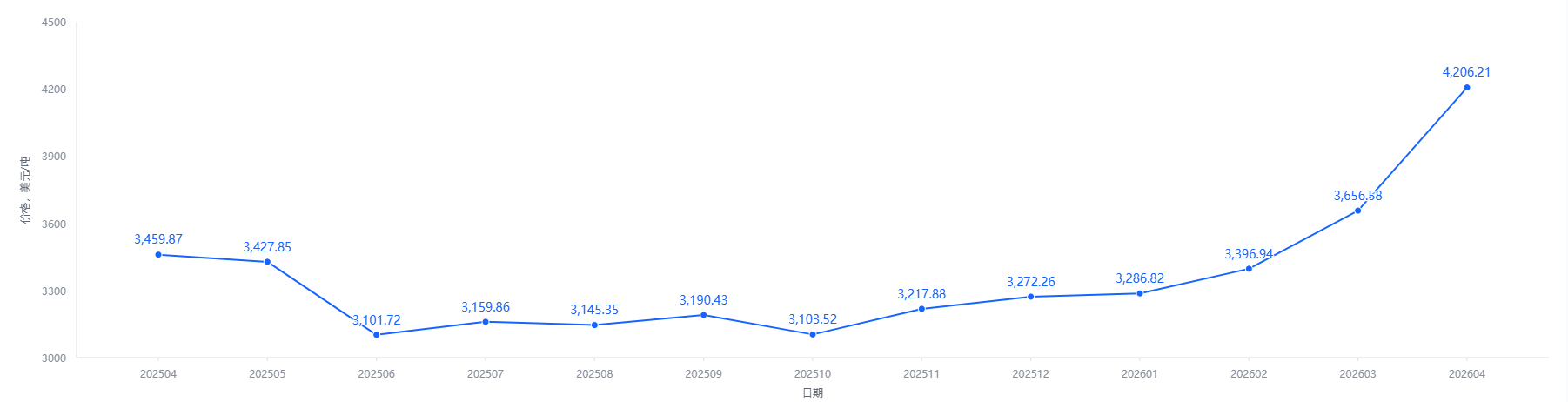

III. Price Trends: Yellow Phosphorus Peaks Then Retreats, Fluctuating at High Levels

Since April 2025, yellow phosphorus prices have shown a three-stage pattern of "volatile upward movement – high-level operation – peak and retreat."

Stage 1 (April 2025 – February 2026): Volatile upward movement. Yellow phosphorus prices climbed steadily from about USD3,459/ton (approximately RMB24,000/ton) in April 2025. High phosphate rock prices and sustained rising raw material costs provided fundamental support.

Stage 2 (March 2026 – mid-April 2026): Accelerated surge. After the Spring Festival and during the spring farming peak season, yellow phosphorus demand accelerated significantly. Industry data showed that by late March, average market prices in Yunnan and Guizhou rebounded more than 8% month-on-month to RMB26,650/ton–RMB26,750/ton, the first increase in three weeks. Entering April, yellow phosphorus ore supply in Yunnan was tight, mining companies were reluctant to sell, and coupled with maintenance at a major Guizhou plant, industry operating rates fluctuated significantly. Yellow phosphorus prices rose for four consecutive weeks to RMB29,750/ton–RMB29,950/ton. After the Qingming Festival, yellow phosphorus prices surged sharply, with downstream just-in-time procurement becoming the dominant market force.

Stage 3 (late April 2026 – present): Peak and retreat. Entering late April, as previously shuttered plants resumed production intensively, operating rates in major production areas increased significantly, and supply gradually expanded. By late April, the average weekly operating rate of yellow phosphorus enterprises in Yunnan rose to around 58%, while the rate in Sichuan rose to around 87%. The increase in supply weakened the core factors that had supported prices earlier, and yellow phosphorus prices began to fall from their highs. According to the latest quotes as of 9 May–11 May, net phosphorus ex-works prices in Yunnan were reduced from RMB28,800/ton to RMB28,500/ton, with the market still under pressure.

Looking at a longer cycle, data from Longzhong Information showed that net phosphorus ex-works acceptance prices in the Yunnan-Guizhou-Guangxi region fell from RMB26,800/ton–RMB27,000/ton to around RMB26,200/ton–RMB26,500/ton in mid-March, reflecting intense supply-demand game.

IV. Corporate Operating Rates and Inventory Dynamics

Operating rates continue to rise, increasing supply pressure.

Since late April, operating rates of yellow phosphorus enterprises in major production areas have continued to increase. As of early May, the average weekly operating rate in Yunnan gradually rose to around 69%, Guizhou around 53%, and Sichuan held steady at around 87%. In April, weekly yellow phosphorus production was about 19,800 tons, with capacity utilization at 63.17%. As previously shuttered plants resume production intensively, supply is accelerating, and the market is gradually loosening.

Corporate inventory management enters a critical phase.

Around the Labor Day holiday, the yellow phosphorus market showed a pattern of contraction on both supply and demand sides. Market feedback indicates that currently, yellow phosphorus enterprises in Yunnan have high operating enthusiasm, but downstream buyers tend to bargain and pressure prices, resulting in sluggish trading sentiment. Data from Longzhong Information showed that during the Labor Day period, yellow phosphorus producers operated well and inventories accumulated steadily. However, before and after the holiday, downstream enterprises replenished stock centrally, releasing significant demand, and producers received considerable orders, driving continuous inventory consumption. Overall inventory increases were relatively small.

From the perspective of raw material reserves for phosphate fertilizer production, major domestic phosphate fertilizer enterprises generally maintained sulfur inventories equivalent to 1.5–2.5 months of consumption during spring farming, ensuring continuous production. As the phosphate fertilizer export ban continues, domestic supply pressure on enterprises will persist, and inventory management will become a key short-term industry issue.

V. Outlook and Industry Views

In the short term, downstream purchasing remains weak around the Labor Day holiday, combined with continued supply expansion in major production areas, so yellow phosphorus prices still face downward pressure. According to Longzhong Information analysis, given the current supply-demand structure and market sentiment, the yellow phosphorus market is expected to continue a weak consolidation trend in the short term, with prices likely to edge down slightly.

From the broader phosphate fertilizer market perspective, the China Phosphate Fertilizer Industry Association noted that upstream raw material markets are highly volatile, and supply chain uncertainty across the entire industry chain continues to increase. Sulfur import dependence is about 50%, and disruptions in the Middle East to sulfur prices remain a core variable affecting phosphate fertilizer costs.

In the medium term, the scarcity of phosphorus resources is becoming increasingly evident. Guotai Junan Securities research report suggests that from 2026 to 2027, the commissioning of iron phosphate production is expected to drive incremental phosphate rock demand of 4.94 million tons and 4.60 million tons respectively, with a tight balance expected in 2026. Meanwhile, demand for industrial-grade monoammonium phosphate from the new energy sector continues to release, and a supply-demand gap is expected to gradually form from 2026 to 2028. The industry is transitioning from a cyclical industry "that lives on agricultural demand" to a growth industry driven by dual engines of "agriculture + new energy."

Data Sources

- CCM (Phosphorus Industry China Monthly Report 202604)

- General Administration of Customs of China (import/export statistics)

- China Phosphate Fertilizer Industry Association (spring farming supply, capacity, industry operating data)

- China Sulfuric Acid Industry Association (sulfur inventory and import dependence)

- Longzhong Information & JLC (daily/weekly yellow phosphorus prices, operating rates, inventory dynamics)

- Guotai Junan Securities Research Report (new energy demand forecast)

- Farmers' Daily (reports on corporate inventory during spring farming)

About CCM

CCM is the leading market intelligence provider for China's agriculture, chemicals, food & feed and life science industries. Founded in 2001, CCM provides price monitoring, trade analysis and customized market research. CCM also offers advertising and promotional services for food ingredient and sweetener suppliers, helping companies enhance visibility and connect with targeted global buyers.

Website: www.cnchemicals.com | Email: econtact@cnchemicals.com | Tel: +86-20-37616606