The January 2026 Monthly Report on China's Sweeteners Industry is officially released. As a core monthly reference for insight into the development of China's sweeteners industry, this report comprehensively sorts out the key industrial development dynamics from the end of 2025 to the beginning of 2026 across six dimensions: Governmental Direction, Project Updates, Corporate Dynamics, Price Trends, Import and Export Trade, and Industry Briefs. The supporting PDF data extract presents key industrial indicators in the form of intuitive numerical tables, price trend charts and export destination pie charts, providing quantitative support for the trend analysis in the monthly report. Based on this report and the supporting data, China's sweeteners industry is now in a development stage featuring expanded policy application boundaries, intensive commissioning of core production capacity, steady recovery of the price market and continuous optimization of export structure. Although demand in some traditional overseas markets has adjusted, the industry's overall development resilience stands out. Meanwhile, the development trends of greenization, diversification and high-endization have become increasingly clear, offering important monthly references for practitioners across the industrial chain to formulate production, trade and layout strategies.

Governmental Direction: Cross-boundary Approval Issued, Expanding Application Scenarios of Sweeteners

The key positive policy disclosed in the Governmental Direction section of this monthly report has become an important signal for the expansion of the application landscape of the sweeteners industry. The Ministry of Agriculture and Rural Affairs (MARA) has officially approved sucralose applied for by Jinhe Industrial as a new feed additive. This approval breaks the long-standing application boundary of sucralose concentrated in the food and pharmaceutical fields, marking the official extension of the application scenarios of domestic sweetener products to the feed sector.

As a new type of synthetic sweetener with high sweetness and low calorie, sucralose features strong chemical stability and a taste close to natural sucrose. Its approval as a feed additive not only brings a new channel for capacity release to leading enterprises such as Jinhe Industrial, but also aligns with the upgrading demand for green and high-efficiency additives in China's feed industry. With the refined and high-end development of the feed industry, the market potential of sweeteners in this field will be gradually released, which also lays a solid policy foundation for the cross-boundary application of other sweetener products in the future and serves as an important new signal for industrial development released in this monthly report.

Project Updates: Multi-category Capacity Commissioning, Enriching the Industrial Product Matrix

The Project Updates section of the report intensively presents the intensive pace of capacity construction in China's sweeteners industry from the end of 2025 to the beginning of 2026. A number of core product capacity projects have been completed, accepted or planned, covering functional sweeteners, synthetic sweeteners, syrups, plant extracts and other sub-categories. The industrial capacity structure is continuously optimized, and the trend of diversified product layout is remarkable.

In the field of functional sweeteners, the Phase I 1,000 t/a HMOs project of Long Health Bio and the Phase I stevia production and processing project of Xinjiang Huijia have been completed successively, catering to the global consumption trend of "sugar reduction and health" and meeting the high-end demand of downstream infant food, functional beverages and health food industries. In the synthetic sweeteners field, the 1,000 t/a neotame project of Meide New Material has been successfully completed, further improving the domestic product matrix of high-end synthetic sweeteners. For syrup products, Anhui Hongchang plans a 3,000 t/a flavored syrup and 8,000 t/a glucose syrup project, which will fill the gap in the diversified demand of downstream food processing and beverage manufacturing. In addition, the completion of the stachyose project of Hebei Jianbao and the proposal of the plant extract and edible-medicine homologous production project by Shenghetang have further extended the industrial product layout towards health and naturalization. The capacity advantages of leading enterprises have become more prominent, and the industry concentration has been steadily improved.

Corporate Dynamics: Dual Drive of Patents & Capacity, Boosting Core Competitiveness of Leading Enterprises

The corporate dynamics disclosed in this monthly report clearly show the development logic of leading enterprises in China's sweeteners industry – building barriers with technological R&D and releasing advantages with capacity commissioning. As an industry leader, Jinhe Industrial has had several patents publicized by the China National Intellectual Property Administration (CNIPA). The patent layout covers the optimization of production processes and product application development of core products such as sucralose, and continuous R&D investment has become the core grasp for the enterprise to consolidate its market position.

At the same time, key projects of many enterprises have successfully passed acceptance checks. The sweetener production project of Sweetmax, the Phase I HMOs project of Long Health Bio and the neotame project of Meide New Material have all completed acceptance, and Xinjiang Huijia has additionally added 1,000 t/a stevia capacity, marking that the new capacity of these enterprises officially has the conditions for release, and their market supply capacity and product market share will be further improved. Technological R&D drives product upgrading, and capacity commissioning realizes technological transformation. This dual-drive model of "patents + capacity" has become the core advantage of domestic sweetener enterprises participating in market competition, and also the core development trend of industrial enterprises reflected in this monthly report.

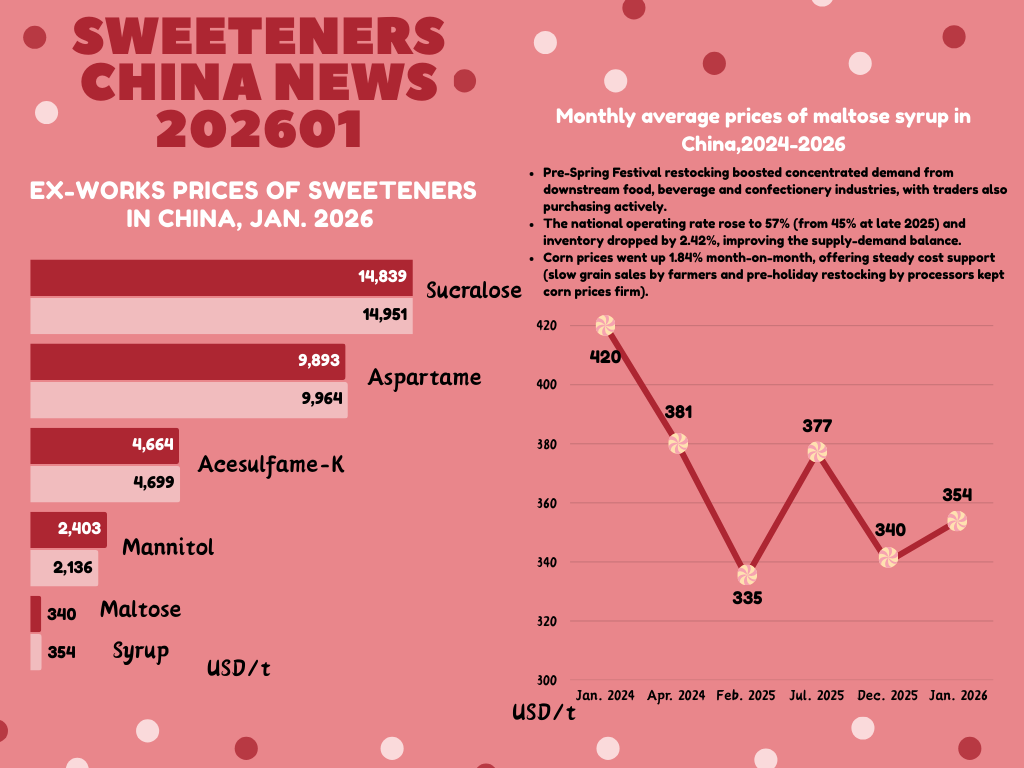

Price Trends: Volume and Price Growth of Core Products, PDF Data Validates Improved Supply-Demand Dynamics

The Price Trends section of the monthly report is the core embodiment of the industrial market recovery, and the precise data refined in the supporting PDF makes the driving factors of price trends more quantitatively based. The January 2026 ex-works price table of sweeteners in the PDF shows that the ex-works prices of domestic core sweetener products remain generally stable. The prices of sucralose, aspartame, acesulfame-K and mannitol are USD 14,951/t, USD 9,964/t, USD 4,699/t and USD 2,136/t respectively. Maltose syrup has become the core highlight on the price side, with its price rising 4.21% month-on-month to USD 354/t, achieving simultaneous volume and price growth.

Combined with the 2024-2026 monthly price trend chart of maltose syrup in the PDF and the analysis of the monthly report, the price rise of maltose syrup is the result of the combined effect of three factors: demand, supply and cost. Before the Spring Festival, the downstream food, beverage and confectionery industries entered the peak stock-up season, and the concentrated procurement demand coupled with active purchasing by traders formed a strong demand support; the national operating rate of the maltose syrup industry rose from 45% at the end of 2025 to 57%, with inventory dropping by 2.42%, highlighting a tight balance between supply and demand; as the core raw material, corn prices rose 1.84% month-on-month, and the slow grain sales by farmers and pre-holiday stock-up by processors kept corn prices firm, providing solid cost support for maltose syrup prices. The stable prices of core products and the volume and price growth of maltose syrup highlight the continuous improvement of the supply-demand pattern in the domestic sweeteners market.

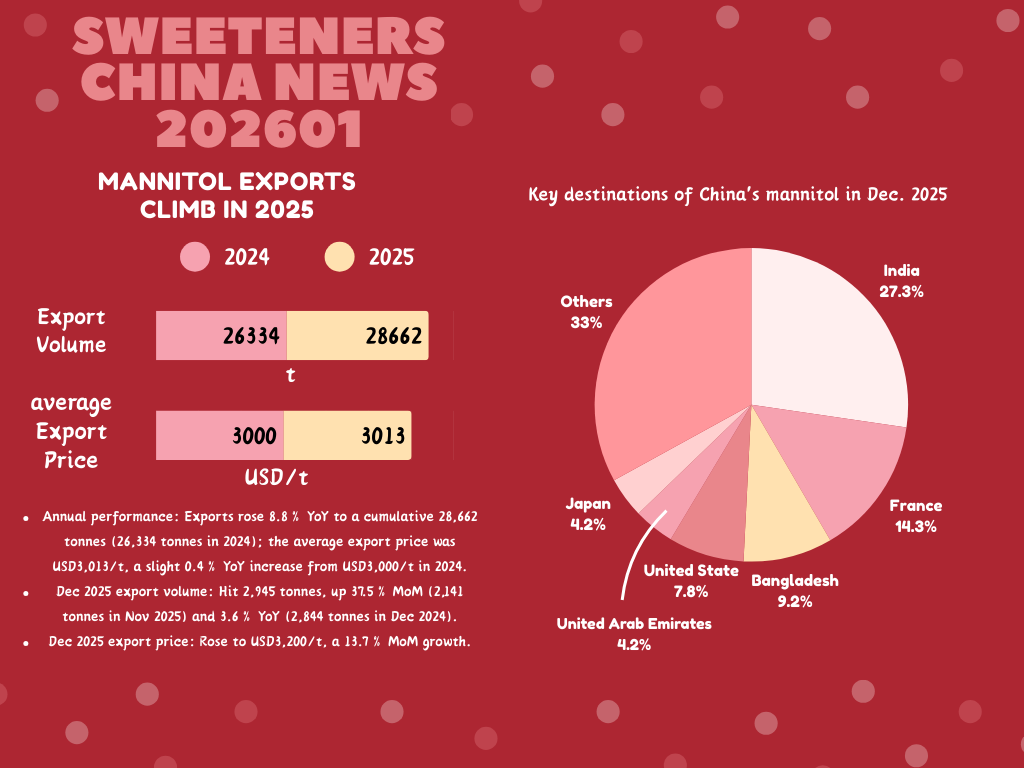

Import and Export Trade: Mannitol Exports Emerge as a Highlight, PDF Data Maps New Changes in Export Structure

The monthly report lists mannitol exports as the core content of the Import and Export Trade section, and the supporting PDF clearly outlines the volume and price performance and market structure changes of mannitol exports in 2025 with specific figures and export destination pie charts, which is the key basis for interpreting the export resilience of the industry. PDF data shows that China's mannitol export volume increased by 8.8% year-on-year in 2025, with a cumulative export of 28,662 tonnes, and the average export price was USD 3,013/t, a slight 0.4% year-on-year increase, achieving both volume and price growth against the background of demand adjustment in some overseas markets. Mannitol exports ended the year strongly in December 2025, with an export volume of 2,945 tonnes (up 37.5% month-on-month and 3.6% year-on-year) and an export price rising to USD 3,200/t (a 13.7% month-on-month increase).

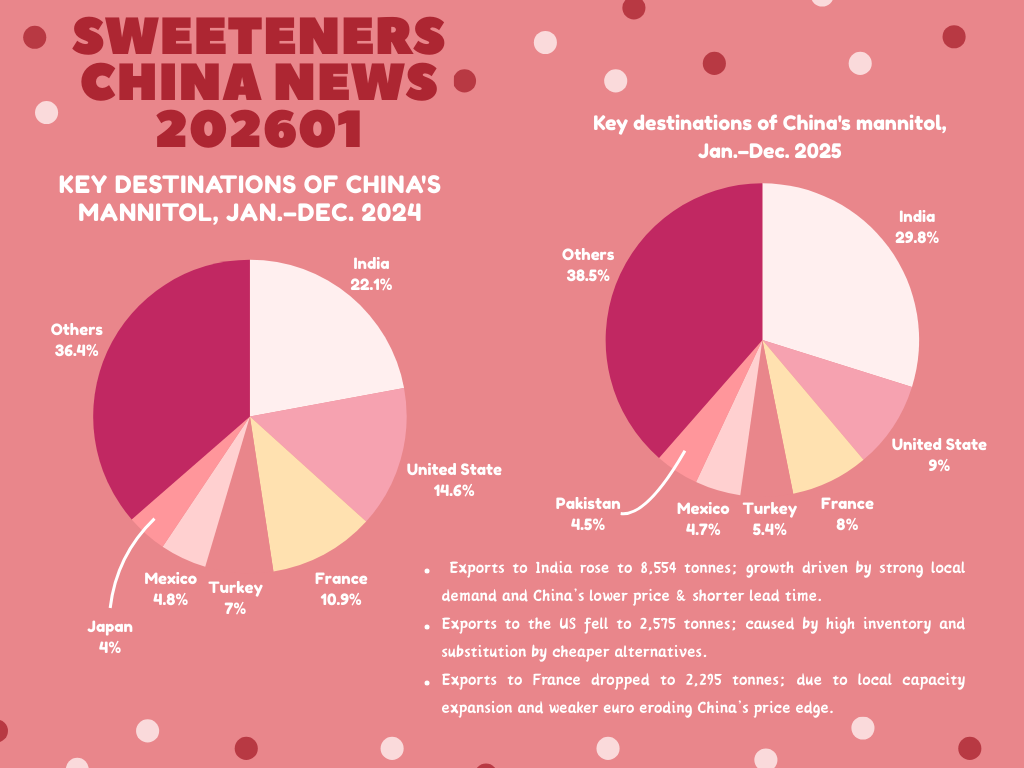

From the export destination pie chart in the PDF, the market structure of mannitol exports has undergone significant optimization, with India emerging as the top growth driver. In 2025, the proportion of exports to India rose to 29.8% for the whole year, with an export volume of 8,554 tonnes, a year-on-year increase of 2,717 tonnes. This is due to the 8%-10% annual growth in demand for mannitol in sugar-free preparations driven by the expansion of India's diabetic population, as well as the high cost-performance advantage of Chinese products with quotes 8%-10% lower than those of the EU and a lead time of only 15-20 days. Exports to traditional markets such as the US and France have declined, mainly affected by high inventory of US pharmaceutical companies and product substitution, as well as capacity upgrading of Roquette Frères in France and the weakening of China's price advantage due to the depreciation of the euro. The strong growth of emerging markets has effectively made up for the gap in traditional markets, becoming a new characteristic of the industrial export structure reflected in the monthly report.

Industry Briefs: All-round Project Progress, Green Development Becomes a Consensus

Although the Industry Briefs section of the monthly report is mainly about project news, it reflects the diversified and green development trends of China's sweeteners industry. The allulose sector has achieved key technological advances; the chicory project of Weinihao and the 5,000 t/a D-xylose project of Jiatai Bio have passed acceptance checks; Yimufangtian has added 50 t/a mogrosides capacity; and starch sugar capacity projects of Hengding Food and Heyun Bio have been launched. These projects cover natural sweeteners, functional oligosaccharides, starch sugars and other sub-categories, further enriching the domestic sweetener product matrix.

At the same time, the environmental impact assessment (EIA) report of Shandong Lanmo's 600 t/a stevioside project has been approved, and Shandong Kanbo's sucrose processing upgrade has realized the conversion of waste acid into hydrochloric acid. This reflects that the industry not only focuses on capacity expansion, but also incorporates green production and circular economy into its development considerations. This not only reduces the environmental protection costs of enterprises, but also improves resource utilization efficiency, aligns with the national "dual carbon" strategic requirements, and makes green development a consensus in the industry.

Core Insights from the Monthly Report: Precise Layout Following Trends to Consolidate Industrial Development Foundations

Based on this January 2026 sweeteners industry monthly report and supporting data, China's sweeteners industry is in a critical stage of high-quality development. Policy dividends, capacity upgrading, price recovery and export optimization have injected strong impetus into industrial development, while challenges such as differentiated demand in overseas markets and fluctuations in raw material prices also exist objectively.

For practitioners across the industrial chain, the core insights from this monthly report are as follows: in terms of market layout, it is necessary to consolidate the share in traditional European and American markets and deeply tap the demand potential of emerging markets such as India and Southeast Asia; in terms of product R&D, focus on the development of healthy, functional and natural sweeteners to cater to global consumption trends; in terms of production and operation, implement green production models, and pay close attention to core indicators such as raw material prices and international exchange rates to adjust business strategies in a timely manner. This monthly report is not only a sort-out of the past development of the industry, but also a prediction of the industrial development trend in the first quarter of 2026, providing an important reference for practitioners to carry out precise layout.