Summary

According to Sweeteners China News 202603, China's starch sugar industry has entered a new round of capacity expansion since 2023. In 2025, new capacity was added across major product lines including crystalline glucose, high-fructose corn syrup, maltose syrup and maltodextrin, with total new capacity reaching around 1.4 million tonnes. This lifted China’s total nominal starch sugar capacity to approximately 25 million tonnes. Expansion is continuing into 2026. As of March, projects under construction or approved had a combined planned capacity of around 2.34 million tonnes, with HFCS remaining the main focus of investment. Meanwhile, low-sugar, sugar-reduction and sugar-free trends are reshaping sweetener procurement among food manufacturers. In the first two months of 2026, China’s sucralose export volume reached a high level, while the average export price dropped sharply, reflecting a market pattern in which demand growth and price competition coexist.

New Starch Sugar Capacity Was Concentrated in 2025

In 2025, China's new starch sugar capacity was concentrated mainly in crystalline glucose, HFCS, maltose syrup and maltodextrin. Shandong Guyu Biotechnology Co., Ltd. added 200,000 t/a of maltose syrup capacity; Inner Mongolia Yuwang Biotechnology Co., Ltd. added 150,000 t/a of crystalline glucose capacity; and Henan Jinyufeng Biotechnology Co., Ltd. added 500,000 t/a of crystalline glucose capacity, making it one of the major crystalline glucose expansion projects of the year.

In liquid syrups, Heilongjiang Donglai Bio-engineering Co., Ltd. added 200,000 t/a of HFCS capacity and 50,000 t/a of maltodextrin capacity. Zhoushan Huakang Biotechnology Co., Ltd. added 100,000 t/a of maltose syrup and 100,000 t/a of HFCS capacity. COFCO Biochemical (Chengdu) Co., Ltd. added 150,000 t/a of F55 HFCS capacity, while Yihai Kerry (Zhoukou) Biotechnology Co., Ltd. added 150,000 t/a of HFCS and 100,000 t/a of maltose syrup capacity.

By the end of 2025, China's nominal annual capacity reached around 6 million tonnes for crystalline glucose, 7.5 million tonnes for maltose syrup, 9 million tonnes for HFCS and 2 million tonnes for maltodextrin. Total starch sugar capacity reached roughly 25 million tonnes. Shandong, Hebei and Heilongjiang remained the key production hubs, supported by proximity to major corn-growing regions and advantages in feedstock supply, logistics and industrial chain integration.

Around 2.34 Million Tonnes of Capacity Is in the 2026 Pipeline, with HFCS Still Leading Expansion

Capacity expansion has not slowed in 2026. As of March, starch sugar projects under construction or approved in China had a combined planned capacity of around 2.34 million tonnes, with HFCS still accounting for the largest share of new investment.

In the HFCS segment, Heilongjiang Longhao Biotechnology Co., Ltd., Yishui Dadi Corn Development Co., Ltd., COFCO Biotech (Pingliang) Co., Ltd., Shandong Taijia Dongheng Biotechnology Co., Ltd. and COFCO Biotech (Taicang) Co., Ltd. are all moving ahead with related projects. New capacity is also planned for maltodextrin, crystalline glucose and maltose syrup, involving companies such as Zhoushan Huakang Biotechnology Co., Ltd., Shandong Dazecheng Biotechnology Co., Ltd., Fujin Liangdu Biotechnology Co., Ltd. and Yumi Biotechnology (Shandong) Co., Ltd.

HFCS has mature applications in beverages, dairy products, bakery products, condiments and foodservice channels. However, as new capacity continues to be released, HFCS is also likely to become one of the most competitive starch sugar categories.

Corn Deep-processing Pressure Is Driving Leading Companies Downstream

The expansion of starch sugar capacity reflects structural adjustments in China’s corn deep-processing industry. In recent years, domestic corn starch and related deep-processing products have faced periodic oversupply. Some large companies have therefore moved further downstream into starch sugar, sugar alcohols, modified starch and other higher-value products to improve feedstock utilization, absorb upstream starch capacity and strengthen product portfolios.

According to USDA FAS' 2026 China Grain and Feed Annual report, China’s corn deep-processing capacity reached around 130 million tonnes by the end of 2025, with more than 70% being starch-based. The sector consumed more than 80 million tonnes of corn in 2025, accounting for around 26% of total corn use. This indicates that starch sugar expansion is closely linked to corn deep-processing capacity, corn prices, corn starch prices and downstream food demand.

For large producers, capacity expansion is not only about increasing supply of a single product. It is also a way to improve the efficiency of the corn processing chain, reduce unit production costs, expand customer coverage and strengthen bargaining power. As a result, industry capacity is expected to become increasingly concentrated among leading producers.

Food Industry Demand Remains, but Capacity Absorption Pressure Is Rising

On the demand side, starch sugars remain important sweetening and functional ingredients for the food industry. HFCS is widely used in beverages, tea drinks, dairy drinks, frozen desserts and condiments. Maltose syrup is commonly used in confectionery, pastries, bakery products, beer and seasonings. Crystalline glucose is applied in food, pharmaceuticals, fermentation and health products, while maltodextrin has stable applications in powdered beverages, nutrition products, milk powder, sports nutrition and meal replacements.

However, the key challenge is that downstream demand growth is slower than capacity growth. As new units come on stream, average industry operating rates may come under pressure, while regional price competition and volume-driven sales are likely to become more frequent. For food manufacturers, abundant supply may improve purchasing power; for producers, profit margins are likely to narrow further.

Low-sugar Trends Are Reshaping Sweetener Procurement

Low-sugar, sugar-reduction and sugar-free trends are reshaping sweetener procurement in the food and beverage industry. China's National Health Commission has emphasized sugar reduction as part of healthy dietary guidance, with daily added sugar intake of no more than 25 grams becoming an important health management target.

This trend has a two-sided impact on the starch sugar industry. On the one hand, traditional channels such as sugar-sweetened beverages, confectionery, bakery products and condiments still require stable, low-cost syrup products suitable for industrial production. On the other hand, food and beverage companies are increasingly using blended sweetener systems to reduce sugar content, driving market attention toward erythritol, sucralose, stevia, allulose and monk fruit sweetener.

In the future, competition in the sweetener market will no longer be limited to price competition between sucrose and starch sugars. Instead, it will move toward integrated competition involving syrups, high-intensity sweeteners, functional sugar alcohols and low-sugar formulation solutions.

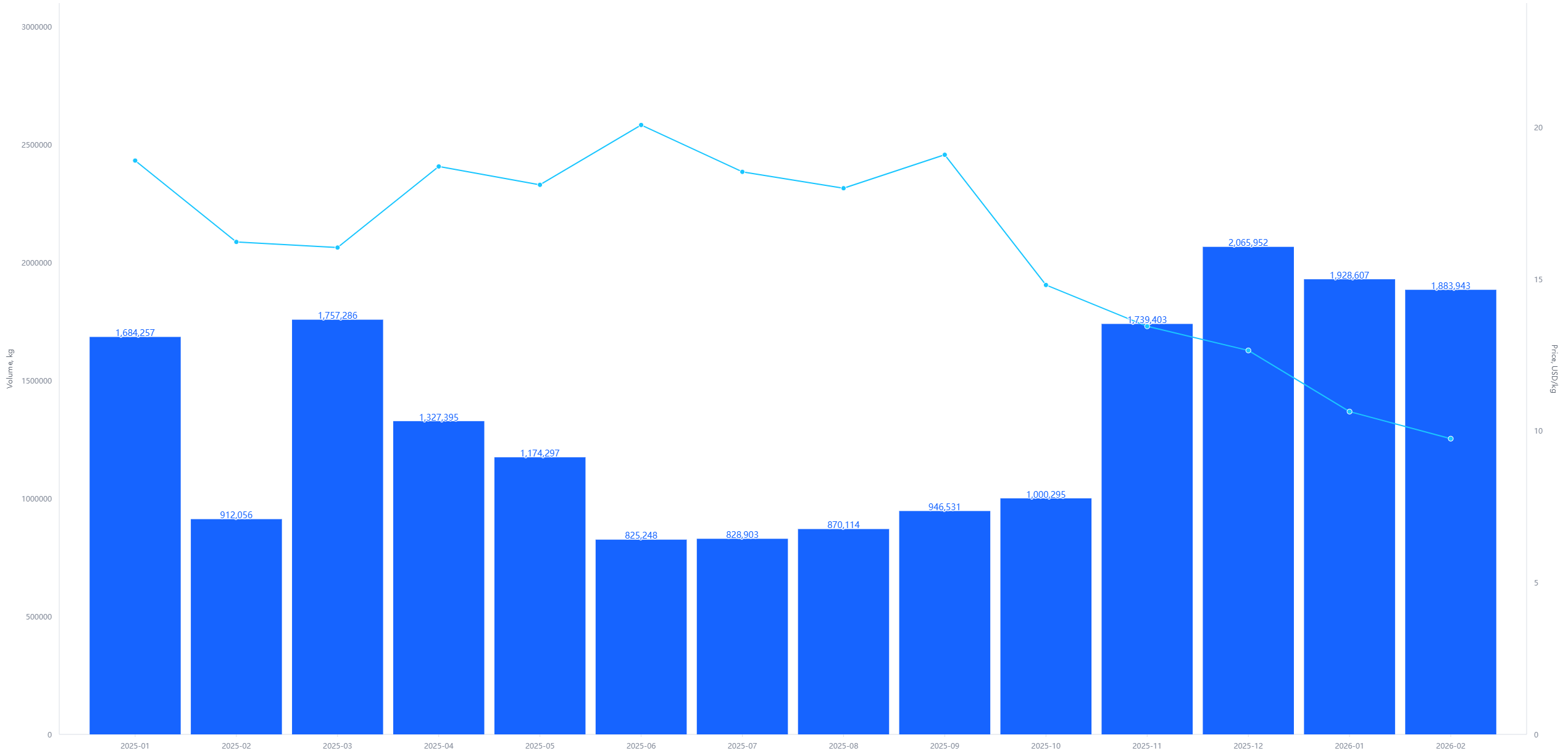

Sucralose Export Volume Reached a High Level, while Prices Fell Sharply

In the first two months of 2026, China’s sucralose export volume rose sharply and reached a high level, while export prices dropped significantly, showing a market pattern of rising volume but falling prices.

In February 2026, China exported 1,884 tonnes of sucralose, up 106.6% YoY and down 2.3% MoM. Export value reached USD18.35 million, up 24.0% YoY and down 10.5% MoM. The average export price was USD9,740/t, down 39.9% YoY and down 8.4% MoM.

During January–February 2026, cumulative sucralose exports reached 3,813 tonnes, up 46.8% YoY. Export value totaled USD38.85 million, down 16.7% YoY, while the average export price fell to USD10,191/t, down 43.2% YoY. Export growth was notable in India, the United States, Ireland, Indonesia, Germany and Uruguay, while shipments to Singapore and Thailand declined.

The increase in sucralose exports was mainly driven by stronger price competitiveness, seasonal restocking by overseas buyers, rising global demand for low-sugar and sugar-free products, and the high concentration of global sucralose capacity in China. By contrast, erythritol exports face more visible trade policy pressure. In January 2025, the European Commission imposed definitive anti-dumping duties on erythritol imports from China, with duty rates ranging from 34.4% to 233.3%, which may affect the export price, customer structure and order stability of Chinese erythritol in the EU market.

Outlook: Price Competition Will Become Routine, with Market Share Concentrating among Leading Producers

Overall, China’s starch sugar market in 2026 is expected to face continued capacity growth, moderate demand expansion and narrower profit margins. As large-scale units gradually come on stream, supply pressure will continue to rise, and new capacity will further squeeze existing market shares.

Large producers are expected to expand their market share through advantages in raw material procurement, large-scale production, logistics networks, customer resources and financial strength. Smaller producers will face higher cost pressure and greater risk of customer loss. Industry competition will gradually shift from pure capacity competition to competition in cost control, product structure, channel coverage, export capability and formulation services.

For food and beverage manufacturers, 2026 may be an important window to reassess sugar sourcing systems, optimize sweetener combinations and lock in reliable suppliers. CCM will continue to monitor capacity, prices, exports and downstream demand in China's starch sugar and sweetener industries through its Sweeteners Monthly Report, export data and market databases.

Data Source

- CCM Sweeteners Monthly Report

- CCM China Starch Sugar Market Monitoring

- Enterprise project announcements, environmental impact assessment disclosures and industry start-up information

- China Customs export data for sucralose, erythritol and other sweeteners

- National Health Commission of the PRC, dietary guidance related to sugar reduction and added sugar intake

- USDA FAS, China: Grain and Feed Annual 2026

- European Commission and Reuters reports on EU anti-dumping measures on erythritol from China

- CCM Market Data and downstream demand tracking for China’s sweeteners and starch sugar sector

About CCM

CCM is the leading market intelligence provider for China's agriculture, chemicals, food & feed and life science industries. Founded in 2001, CCM provides price monitoring, trade analysis and customized market research. CCM also offers advertising and promotional services for food ingredient and sweetener suppliers, helping companies enhance visibility and connect with targeted global buyers.

Website: www.cnchemicals.com | Email: econtact@cnchemicals.com | Tel: +86-20-37616606