Summary

In the first quarter of 2026, China's fungicide technical market exhibited a pattern of subdued consolidation and bottoming stabilization. Ex‑works prices of core active ingredients, notably azoxystrobin and tebuconazole, edged slightly lower. However, heading into late March, with the gradual release of spring planting demand and emerging cost support from upstream inputs, signs of a market bottom are accumulating. Drawing on CCM price monitoring data, this article examines the evolving supply‑demand landscape against the backdrop of spring disease pressure, capacity expansion, and export trends, and provides an outlook for the second quarter of 2026. This analysis is based on core data and insights from CCM's Fungicides China Monthly Report 202603.

Key observations from the data:

-

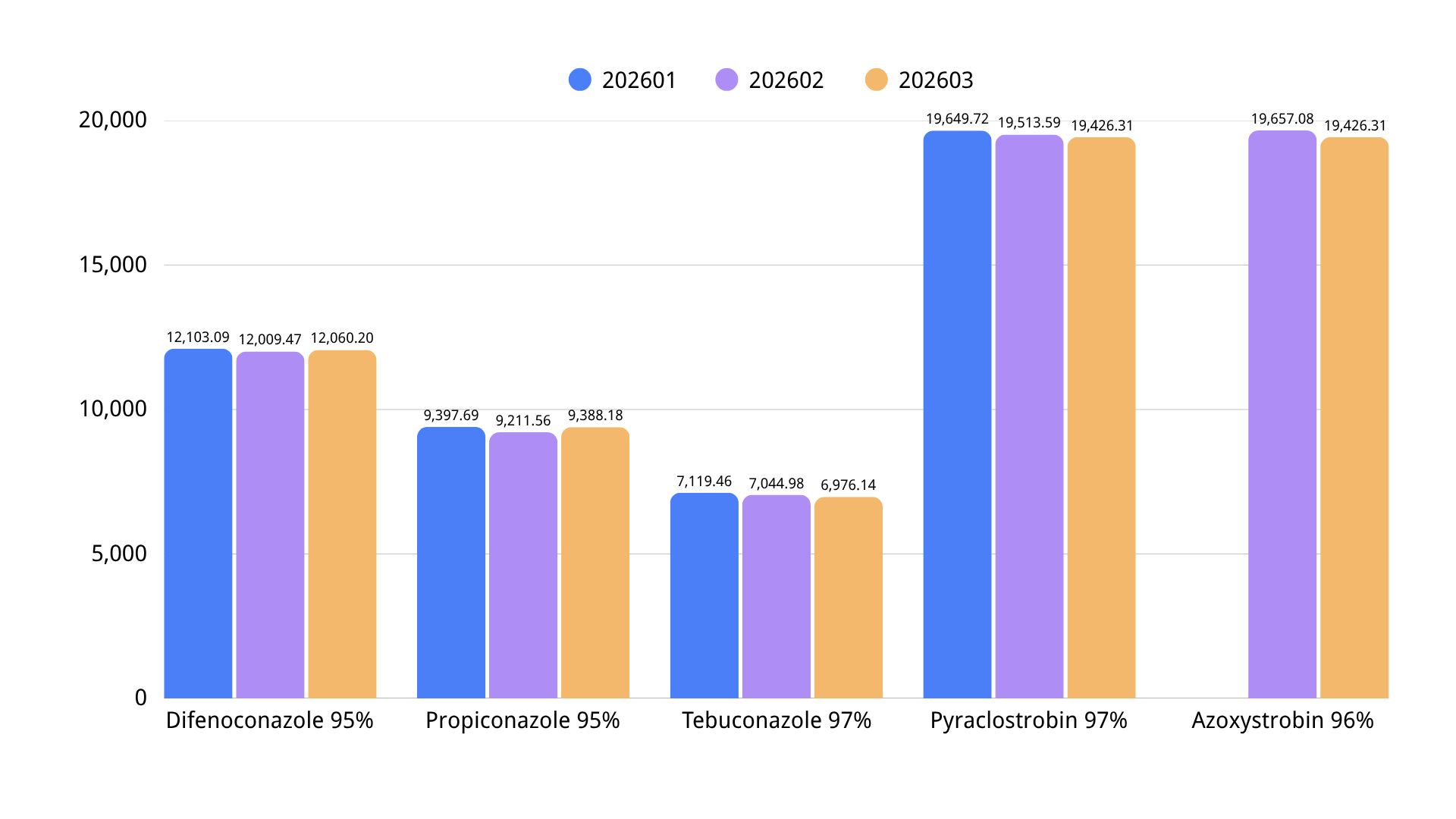

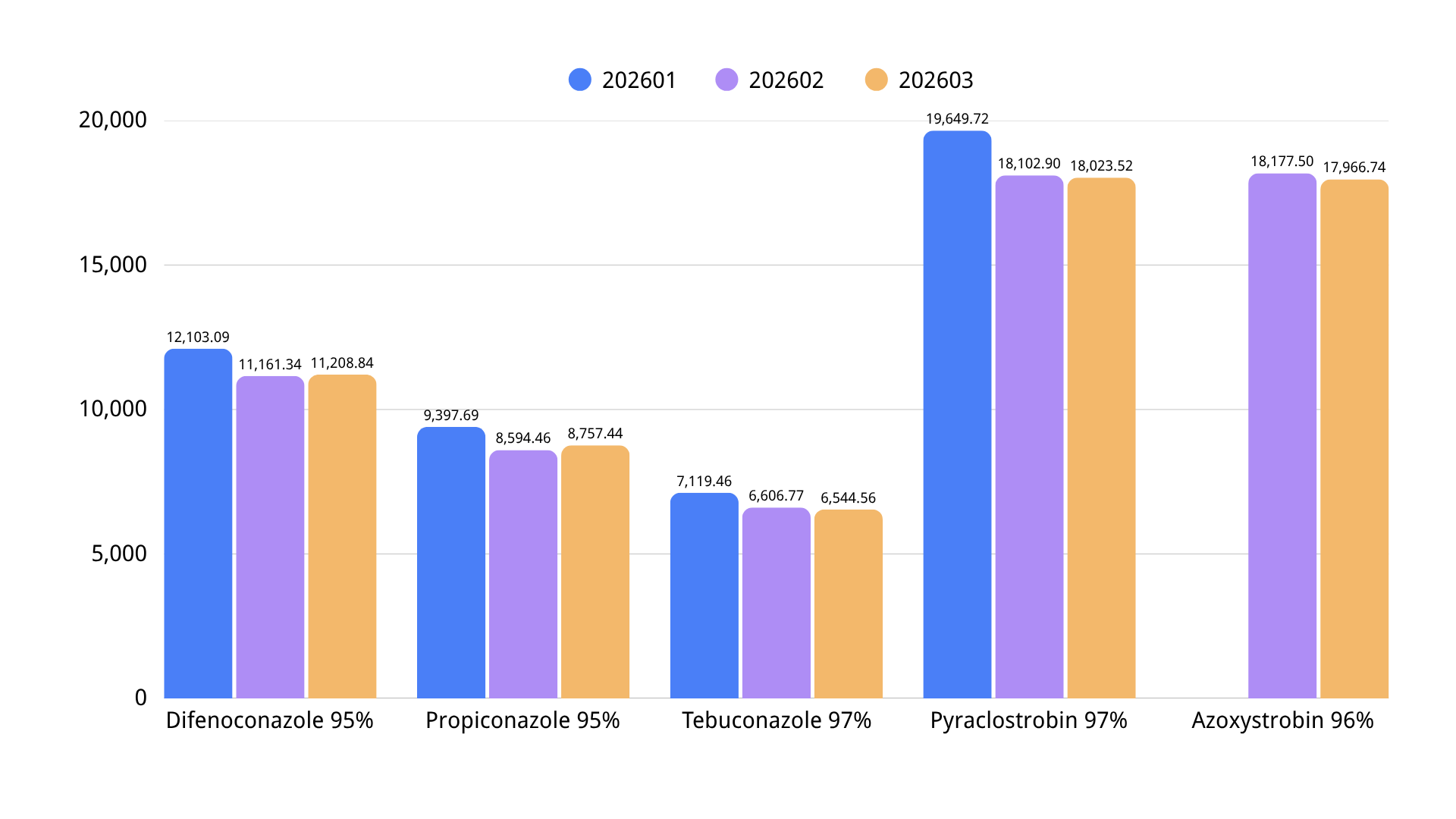

Azoxystrobin 96% TC: Ex‑works price stood at RMB 19,657.08/tonne in February, edging down to RMB 19,426.31/tonne in March. Ample market supply and the absence of a concentrated demand surge kept prices under mild pressure, although the pace of decline has visibly moderated.

-

Tebuconazole 97% TC: Quoted at RMB 7,119.46/tonne in January, RMB 7,044.98/tonne in February, and RMB 6,976.14/tonne in March—a cumulative Q1 decline of approximately 2.0%. The broader triazole segment remained subdued, with cautious downstream restocking contributing to a gentle downward drift in price levels.

-

Difenoconazole 95% TC, Propiconazole 95% TC, and Pyraclostrobin 97% TC: All exhibited similar mild retreats or range‑bound movements, reflecting generally lackluster trading activity.

Despite the soft price performance in Q1, marginal improvements emerged in late March. On one hand, persistently elevated prices of key upstream intermediates provided growing cost support. On the other, several manufacturers suspended external price quotations, indicating diminished willingness to offer further concessions at current low price levels. Signs of a price bottom are accumulating, setting the stage for a potential recovery in the second quarter.

II. Heightened Spring Disease Pressure Means Rigid Demand Is Only Deferred, Not Canceled

According to comprehensive analysis by the National Agro‑Tech Extension and Service Center (NATESC) in collaboration with provincial plant protection agencies and research institutions, major wheat pests and diseases are expected to be moderately to severely prevalent in 2026, covering an estimated 810 million mu‑times. Disease occurrence accounts for 480 million mu‑times, while pest occurrence accounts for 330 million mu‑times. Fusarium head blight (FHB) poses a high risk of moderate to severe epidemics in the middle and lower Yangtze River, Jianghuai, Huang‑Huai, and southern North China wheat regions, with an estimated affected area of 140 million mu and a required preventive treatment area of 250 million mu‑times. Wheat crown rot is forecast to occur at a moderate level in the Huang‑Huai and southern North China wheat regions, covering approximately 51 million mu.

Phenologically, the majority of winter wheat in the Yangtze River basin is currently at the flowering stage—a critical window for FHB control. NATESC has explicitly designated triazole fungicides such as tebuconazole as recommended agents for controlling FHB, rust, and powdery mildew. The elevated disease pressure underscores that end‑use demand is only delayed, not eliminated. As regional governments roll out "one spray, three preventions" procurement programs, channel restocking demand is poised for concentrated release in April and May, providing strong impetus for upstream inventory drawdown.

III. Azoxystrobin: Subdued Price Consolidation Amid Capacity Expansion and Export Expectations

Counterbalancing the modest price erosion in Q1, domestic azoxystrobin capacity expansion continues unabated. Jiangxi Lianbai Technology Co., Ltd. has officially advanced its 1,500‑tonne/year azoxystrobin technical upgrade project in the Wannian High‑Tech Zone, Shangrao, with plans to further expand capacity to 3,000 tonnes/year. Nantong Taihe Chemical's 5,000‑tonne/year integrated azoxystrobin project is scheduled for trial production in 2026, while Inner Mongolia Lingsheng Crop Science has obtained filing approval for a 10,000‑tonne/year azoxystrobin facility—the largest single‑unit capacity currently in the pipeline. Over the medium to long term, supply is set to become more abundant.

Nevertheless, the export market continues to provide a floor under prices. Azoxystrobin export orders for 2025 were already booked through year‑end, and demand from key markets such as Brazil and Southeast Asia remains steady. Current ex‑works prices for azoxystrobin are approaching the industry's average cost line, limiting further downside. As both domestic and overseas demand pick up in Q2, prices are likely to stabilize and gradually recover.

IV. Tebuconazole: Early Signs of a Price Bottom as Inventory Pressure Eases

Tebuconazole prices declined by approximately 2.0% cumulatively in Q1, but the month‑on‑month drop narrowed markedly in March, indicating waning downward momentum. According to CCM monitoring, several major tebuconazole producers—including Jiangsu Sword Agrochemicals, Jiangsu Huanghai, and Yancheng Huihuang—have suspended external price quotations since late March, signaling firmer pricing resolve in the face of cost pressures. Meanwhile, downstream channel inventories have been drawn down to relatively low levels over the winter, and rigid restocking demand is poised to materialize as the peak season for wheat FHB control approaches.

From a supply‑demand balance perspective, tebuconazole inventories are gradually being absorbed, and the market is transitioning from "ample supply" toward a tight balance. Once end‑use demand kicks in forcefully, tebuconazole prices have a strong probability of rebounding.

V. Export Market and Outlook

The export sector remains a crucial pillar of support for the fungicide market in 2026. Industry estimates suggest China's total pesticide export volume grew by approximately 16%–18% year‑on‑year in 2025. Brazil, as its soybean and second‑crop corn planting seasons advance, continues to exhibit robust import demand for fungicide technicals. Southeast Asia's crop mix provides consistent support for triazole and strobilurin products.

On the policy front, the Ministry of Agriculture and Rural Affairs fully implemented the "One Certificate, One Product" policy effective January 2026. By strengthening the linkage among product registration, trademark, and manufacturing entity, the policy compels companies to pivot from private‑label competition toward R&D‑driven innovation. Industry consolidation is expected to accelerate, further advantaging leading enterprises.

In summary, the Q1 2026 fungicide market was characterized by price bottoming and demand accumulation. Although ex‑works prices drifted modestly lower, three converging forces—cost support, inventory drawdown, and rigid disease‑control demand—are building momentum. As the peak season for pest and disease control in rice, corn, and other key crops arrives in Q2, demand for azoxystrobin and tebuconazole still has room for expansion, and a stabilization or recovery in prices appears increasingly probable.

CCM will continue to monitor the latest fungicide market developments, delivering comprehensive market intelligence services covering ex‑works prices, FOB prices, inventory levels, trade flows, and competitive landscape analysis—empowering industry participants to navigate market trends and make informed strategic decisions. For more detailed data and analysis, please refer to the Fungicides China Monthly Report 202603.